Economic modeling and studies: machne learning is applied to intraday optimization and trading in Germany

11/01/2017News

ENGIE’s Center of Expertise in Economic Modeling and Studies (CEEME), in collaboration with the GEM BU, has developed a concrete machine learning application for intraday optimization and trading in Germany.

Driven by the growth of renewable sources of energy, intraday electricity markets are becoming increasingly important on the trading floors of the major energy groups. Intraday enables generators to meet their electricity supply commitments when production and/or consumption deviates from their day-ahead forecast (since generation plans must be submitted to the power exchanges no later than noon the day before).

“Machine learning is a highly promising field of study in artificial intelligence, specifically when applied to trading and optimization,” stated Olivier Lecointe, CEEME Director.

German intraday market: a fertile ground for strategies based on machine learning

The German intraday market exhibits several characteristics that make it particularly well suited to the development of automated trading and optimization strategies:

- A Physical market, with very little speculation

- Price movements are often the result of measurable fundamentals, the volumes involved are relatively low

- Many players involved

Numerous factors can trigger large intraday price movements:

- Changing weather forecasts

- Unscheduled unavailability of generation units

- Status of the transmission grid

- Flexibility of generating facilities

Given this context, machine learning is useful for detecting and exploiting market situations in which intraday prices differ from their expected behavior, and which would not be possible to spot using conventional statistical approaches because there are too many variables simultaneously influencing price formation.

Detecting opportunities for gains via a machine learning algorithm

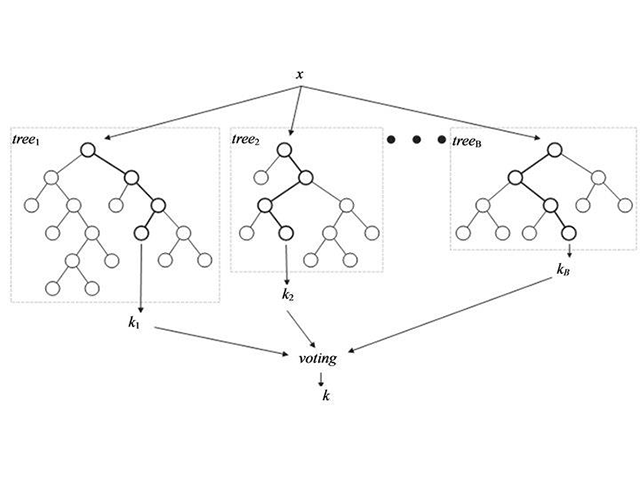

Machine learning makes it possible to detect combinations of factors in which a sought-after phenomenon is observed statistically. The aim is to detect market situations in which prices deviate significantly from what a model predicts. This model is built by learning the relationships between observations of recent months or years. The figure below illustrates how to combine several trees to increase the predictive capabilities of the model.

After a long iterative process of data mining and modelling, we were able to correctly predict the direction of price trends in around 57% of the cases. This may seem low at first glance, but it is a quite remarkable score in this context of market analysis.

The teachings of models

Machine learning algorithms are currently being tested in production to determine if they deliver satisfactory results in a real-world setting.

By analyzing the frequencies of occurrence of the different variables in the trees (as well as their respective position in those trees), they can be classified in decreasing order of relative influence:

- Residual load

- Quantity of wind generation anticipated on a day-ahead basis

- Trend in intraday prices observed in the quarter-hour preceding the decision

- Total deviation (compared to the day-ahead) of renewable generation forecasts (wind + solar) four hours before the product expiration

- Quantity of solar generation forecasted in day-ahead

- Hour of the product

- Deviations in renewable generation announced in the hour preceding the decision

- Time remaining until expiration of the product

- Spread between the intraday price and the day-ahead price, three hours before the decision

- …

The study has revealed one of the most interesting aspects of machine learning: the ability to use data to truly understand the intraday price dynamics.

> For more information, contact Olivier Martin (CEEME): olivier.martin@engie.com